- Get in Touch with Us

Last Updated: Jul 16, 2025 | Study Period: 2025-2031

Over the past few decades, agriculture hasevolved into a highly diverse and complex sector globally, with operational units ranging from small and sustenance-based farm holdings to large corporate farm holdings. With the rise in population, food insecurity and malnutrition have been posing serious challenges at the global level, especially in developing economies.

At the current and forecasted growth rate pattern, the world's population is projected to reach nearly 10 billion by 2050.

In addition to agricultural, social, and economic growth drivers of mechanization, macroeconomic and intrinsic factors such as the growing population and demand, urbanization, surge in Agri exports such as tractors, improved flow of agricultural credit, labor migration, and shortages are also necessitating the adoption of mechanized solutions

Mahindra Digisense 4G, a farmer's third eye is the Next-Gen AI ( Artificial Intelligence) driven open Architecture connected solution which helps farmers track their tractors and control their farming activities remotely.

It aims to empower farmers with data on their farming operations, which in turn will enable them to make more profitable decisions. The features of this technology were location services, security, farming operations, productivity, vehicle health, maintenance, personalization, and configuration properties.

John Deere has unveiled its first self-driving tractor, which can be controlled by farmers using a smartphone and run 24 hours a day. The company will deliver up to20 machines in 2022, with a scaled-up rollout in the coming years -Jan 2022

Sonalika Tractors launched its most advanced Tiger DI 75 4WD tractor with superior CRDs (Common Rail Diesel System) technology for an introductory price range of Rs. 11-11.2 lacs.

Designed to deliver the industry-first dual benefit of power and economy, the Tiger 75 4WD with CRDs technology complies with Trem IV emission norms and offers the power of 75 HP & economy of 65 HP tractor-December 2021

Solectrac launches a New e70N e-tractor for California farmers and vineyards, a specially designed narrow model purpose-built for easy handling and maneuverability on farm operations.

The Solectrac e70N tractor is a 4WD, 70 HP with up to eight hours of operation from a single charge and the ability to extend that time via a swappable battery pack to work more efficiently '“August 2021

TAFE introduced its Massey Ferguson 244 DI '“ Puddling special tractors in the 44 HP range for paddy cultivation with two variants MF 244 DI PM for dry land or shallow pudding applications and MF 244 PD for deep mud puddling '“July 2021

TAFE launched Dynatrack tractors which have an extendable wheelbase for agricultural, haulage, and commercial applications and offer maximum ground clearance for all-terrain operations including puddling and easy crossing of bunds '“February 2021

The SA line of versatile compact tractors from Yanmar America Corporation has been updated. The brand-new SA series guarantees precise control with an exceptional blend of strength and effectiveness.

All-new SA223 models from Yanmar have a net power of 19.4 HP, SA325 models have a net power of 21.7 HP, and SA425 models have a net power of 21.7 HP. All models include Yanmar's 10-year/3000-hour limited powertrain warranty and are assembled in Yanmar's cutting-edge Adairsville factory in the United States.

Performance improvements include dual range speeds, standard differential lock, and Yanmar's exclusive True Position Control technology for precise and accurate control of implement operating height are all part of the SA series. - June 2022

The world's largest tractor producer by volume, Mahindra Tractors, a division of Mahindra's Farm Equipment Sector, today revealed six new tractor models under the recently established Yuvo Tech+ brand. Mahindra's Research Valley (MRV) in Chennai is where Mahindra Yuvo Tech+ was created, using top-notch standards. New m-ZIP 3-cylinder and ELS 4-cylinder engines from Mahindra Tractors provide the best-in-class power, torque, and mileage for the new tractors.

The six new models are part of an expansion of the Yuvo Tech+ lineup and are available in the power range of 37 to 50 HP (27.6 to 36.7 kW). They have crucial features including 4-wheel drive, Dual Clutch, SLIPTO, Auxiliary Valve, and 2-speed PTO, making them suited for more than 30 agro applications. - July 2022

The seventh generation of Fendt 700 Vario series tractors is coming to North America from AGCO Corporation, a leader in the design, production, and sale of agricultural machinery and precision ag technologies. Its best-selling range now includes a new design, engine, and technological advancements.

Five different variants of the Fendt 700 Vario tractors are offered, with engine horsepower ratings ranging from 203 to 283. Each model includes the quality, comfort, and adaptability that Fendt customers have come to expect. When farmers require more power, the Fendt DynamicPerformance (DP) extra power concept in the Fendt 728 Vario DP accurately releases up to 20 more horsepower via a demand-dependent control system.- August 2022

The tractor industry entirely depends upon the agricultural industry and factors such as the economy, adverse weather, farm input costs, and lower commodity prices, have been badly affected by COVID-19 which has directly affected the tractor industry.

High Diesel prices in India have already increased the operation cost of farmers who have been battling with various other financial issues. This is an important risk to the market.

Electrification and autonomous features are the way forward for the tractor industry much like the auto industry. In Jan 2020, Kubota introduced an unmanned X Tractor, which is not only electric but also smart enough to determine the best time for planting and collecting plants.

At GaLaBau in Nuremberg and Salonvert near Paris this year, Yanmar Europe will announce a New 5-Year Warranty for Yanmar SA, YT2, and YT3 Utility Tractor Series from 22 to 60 hp.Compact tractors' lifecycle value is significantly increased by the new extended warranty policy, which maximizes performance and efficiency while lowering expenses and downtime.

Zimeno Inc. and Hon Hai Technology Group have signed a contract manufacturing agreement (CMA). At the Foxconn site in Ohio, DBA Monarch Tractor will produce battery packs and the newest agricultural machinery.

In order to meet the rapidly rising demand in North America, Kubota Industrial Equipment Corporation (KIE), a U.S. subsidiary of Kubota Corporation, will construct a new plant to produce work equipment for mounting on tractors.

Front-loaders for hauling items like mud and hay, backhoes for digging, and other equipment are frequently included with new tractors that are marketed in North America.More than 90% of these tractors are front-loader-ready. The annual implement production capacity will be increased from 100,000 units to 210,000 units by the new and existing plants in response to the enormous North American demand.

Mahindra Tractors, part of Mahindra & Mahindra Ltd.'s Farm Equipment Sector, presented "OJA" as the new brand name for its new future-ready range of tractors from its most ambitious global tractor program, K2.

The Mahindra OJA is Mahindra's all-new lightweight global tractor platform, focusing on both domestic and international markets such as the United States, Japan, and South-East Asia.It was developed in close collaboration between the engineering teams of Mitsubishi Mahindra Agriculture Machinery in Japan and Mahindra Research Valley in India, Mahindra's Auto & Farm sector's R&D center.

Mahindra's Zaheerabad tractor factory, a vertically integrated tractor facility, also produces Mahindra's next-generation Yuvo and Jivo tractors, including the recently announced Plus Series of tractors. The Zaheerabad plant is highly advanced, having the ability to produce approximately 330 distinct tractor variations ranging in horsepower from 30 to 100 hp.

In June 2021, U.S. tractor sales declined 12.7% which was only the second negative result in a year while U.S. self-propelled combine sales rose 4.1%.Tractors below 40hp (29.8kW) fell 18.4%, leading to an overall decline in sales for the month. The mid-size segment, 41-100hp (30.6-74.6 kW), also dropped slightly.

In June 2021, U.S. farm tractor inventory (71,035) is 41.3% below the same month in June 2020(121,169), while Canadian inventory is down 33.2% over that same time (9,535 in 2021 to 14,288 in 2020)

All other segments were positive, with the articulated 4WD segment leading the way for the second straight month by more than doubling, up 141.8% to 266 units sold. The 100+ hp 2WD segment also grew 24.8%. Year to date farm tractor sales remain up 16.7% and combined up 11%.

Row-crop tractors and harvesters mostly used in commercial farming operations have shown a decline which can be attributed to the reflection of the uncertainty in the overall agricultural economy.The net farm income has been falling in the past six years and almost halved to $63 Billion in 2018 from ~$123 Billion in 2013.

To know more about theFarm tractor market in the U.S, read our report

The first quarter of FY22 was tough for the Indian tractor market due to the nationwide lockdown. Despite that, the total domestic tractor sales were recorded 2,29,441 units in Q1 FY22 which is 38.92% more than the domestic tractor sales in Q1 FY21 where the sales recorded in Q1 FY21 were 1,65,156 units.

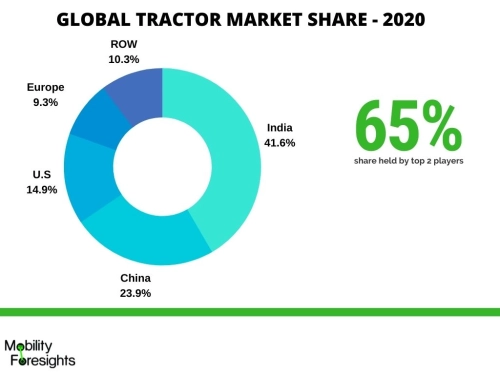

India is the world's biggest tractor market with over 899k units sold in FY 2020-2021.

India's tractor market has come out unscathed as the COVID pandemic rages within the country. Rural markets are leading the rebound even as many urban and semi-urban centers remain under partial lockdown.

The tractor market is also insulated from the ongoing 'œboycott China' sentiments as it has negligible dependence on China for components. Almost 95% of components are produced locally.

After implementing BS6 emission norms (equivalent of Euro 6) for the auto industry, the tractor market is now gearing up to adopt BS TR-Tractor EM-Emission (TREM) 4 norms (for tractors over 50 HP) by October 2021.

The switch to BS TREM 4 could impact ~7-10% of overall industry volumes in the fiscal year, as the prices are likely to go up by $1,800 -$2,500 per tractor. The tractors below the 50 HP segment will migrate to the new norms by October 2023.

On the manufacturer's side, the migration to the new norms would require up-gradation of the fuel injection system, exhaust after-treatment and the electronic control unit costing ~$2 Million per manufacturer per engine type.

To know more about the Farm tractor market in India, read our report

In Italy, the farm machinery registrations were up during the first quarter of 2021. Tractor registrations rose 57.7% while combine harvesters increased 180% due in part to tax incentives from the government as well as demand for next-generation technology.

The German Tractor market sold 26,209 units year-to-date in 2021 compared to 19,581 units sold in 2020. Factors like superior productivity through mechanization and labor deficiency have led to the expansion of the agricultural equipment demand in Germany, as the shortage of labor has increased the demand for tractors.

In Germany, tractor sales grew by 2.6% YOY to finish at 29K units. More than 74% of overall sales was for Tractors with more than 50HP output. Similarly, the Turkey tractor market sold 22,232 units year-to-date in 2021, an increase from 14,574 units sold in 2020.

In the UK very few tractors are made locally, CNH Industrial's New Holland plant in Essex and JCB's Fastrac plant near Cheadle, Staffordshire are the only two important manufacturing locations in the UK.

The UK sources various high-horsepower models from the US. UK tractor registrations in June 2020 declined by 15% YOY. Many tractor production plants have started production post-lockdown, although at a much lower capacity.

To know more about theFarm tractor market in Europe, read our report

China`s farm mechanization rate is estimated at 69% in Q1-2021. It is still low as compared to developed markets and that is where a big opportunity lies. On the flip side, domestic Chinese farmers and other countries will directly benefit from this move.

China's agricultural machinery sector is big in terms of volumes but underdeveloped in terms of technology. Until recently, most Chinese manufacturers only manufactured low-end equipment which finds buyers in the domestic market and a few African markets.

They were not well suited for exports to the US or Europe. But in the recent past, there have been heavy investments made by European and American manufacturers.Earlier, to plug this gap in high-end equipment, many Chinese farmers get used agricultural equipment from the US and Europe at lower prices.

To know more about theFarm tractor market in China, read our report

In 2021, Due to the pandemic, the 2WD tractor transmissions hold a negative growth resulting in fewer tractor overall sales. Nearly over ~ 97-98% of 2WD tractors are sold globally.

4WD tractors are more suitable for large farmlands with high flexibility on many farm operations. By 2026, the volumes will grow 50% compared to 2020. As the product offering and customers shift to automatic transmissions.

The Global Tractor market was valued at approximately USD 79.3 billion in 2024 and is projected to reach USD 108.6 billion by 2031, growing at a CAGR of 4.6% during the forecast period.

The global tractor sales volume was ~2.03 Million units in 2020 a rise of 6.8% compared to 1.9 Million units in 2016.

A fully autonomous tractor, one of the most cutting-edge agricultural products of the year, was unveiled by John Deere. The device combines the 8R tractor from the company, a chisel plough with TruSet functionality, a GPS guidance system, and new, cutting-edge technologies. Six stereo camera pairs on the tractor detect obstacles, measure distance, and constantly monitor their location in relation to a geofence.

Farmers only need to move the tractor to the fields and set it up for autonomous operation using the John Deere Operations Center in order to use it.Once it is set up, the farmer can monitor the machine from their mobile device while they are away from the field and concentrating on other tasks.

The first fully electric, driver-optional, smart tractor built on a single platform was unveiled by Monarch Tractor today.Labor shortages, the effects of climate change, safety concerns, increased customer scrutiny for sustainability demands, government regulations, and other issues are just a few of the difficulties farmers today face.

In order to improve farmers' current operations, boost labour productivity and safety, and maximize yields to reduce overhead costs and emissions, Monarch Tractor combines electrification, automation, machine learning, and data analysis. The business has already signed up several hundred working farms as clients.

It also functions as a three-in-one electrification tool, acting as a tractor, an ATV with additional storage, and a powerful generator in the field when necessary. Without a driver, the tractor can carry out pre-programmed tasks, or an operator can use interactive automation features from Monarch, such as Shadow and Gesture modes, to have the tractor follow a worker while they work.

Tractors have come a long way since they were invented in the late 1800s. Here are some of the most recent tractor technologies and trends:

COVID-19 has affected various sectors across the world. Among these, one of the major fields affected by it, is the Tractor Sector. This sector has seen a sharp dip in the tractor business, and the most affected business could be the dealership network due to the disruption of the supply chain and manufacturing units were not 100% active.

Due to lockdown and travel restrictions by the governments, production of goods got delayed, as supply was interrupted, resulting in a sharp decrease in tractor sales during this pandemic. Besides lockdown , the industry has also been hit by supply logjam just in the middle of the harvesting season.

This is a boom time for tractor sales, but the sector is scrambling to keep up production because of the disruptions all along its supply chain, including the short supply of tyres.

Unlike in the first wave of COVID-19 where the impact was not at all there in the rural market, but with the second wave of COVID-19 pandemic hitting rural areas, tractor sales were impacted in the short term although in the second half of fiscal year it is likely to pick up to give the industry a mid-single digit growth.

However, in the later phases, the demand for agricultural machinery, including tractors, increased due to higher Kharif sowing, good cash flows to farmers, a timely and normal monsoon in the world across June and July, continued higher rural spending by the government and exemption from lockdown restrictions. Hence, there is no impact on the tractor market due to the global pandemic.

The Government of India took initiatives regarding rural development and farm mechanisation such as enhancing rural wages and scarcity of farm labour are likely to increase the tractor volume over the long term in India.

The government also took certain steps to plummet the spread of the coronavirus and enhanced the tractor sector directly by reducing the tax of the raw materials and amended the farmer's bill which indirectly increased the demand of the tractors and would have a great access to more sources of income.

Regarding the measures taken by the Government of India, the tractor sector had reported the records in FY 2021 despite the pandemic impact having a largely flattish volume this year which is higher than the previous year.

The innovative Solis Hybrid 5015 tractor with Japanese hybrid technology was launched by International Tractors Limited (ITL), the manufacturer of Sonalika tractors.This novel hybrid tractor was created in partnership with Yanmar Agribusiness Co. Ltd. in Japan to provide the benefits of three tractors in one.

The business claims to be the first tractor manufacturer in India to introduce 'E-Powerboost,' a Japanese hybrid technology, as part of its Solis Yanmar range, and claims to have patented the related product advancements. Hybrid tractors come with innovative features like E-Powerboost, which allow the farmer to have the power he needs when he needs it and maintain fuel efficiency while running as a standard tractor the rest of the time.

Claas is introducing the Terra Trac friction drive track from its combines to the Axion 900 tractor series with the Axion 900 TT, the company's first half-track tractor with full suspension.The new Trion 740 combine, a Class 7 machine designed for small to medium-sized farming operations with a focus on maize and soybean output, was also unveiled.With its driving track, the new Axion 900 TT is designed for improved flotation, traction, operator comfort, and soil protection.

The Terra Trac on the 900 TT also includes a larger rear driver wheel, which improves the surface area of contact between the plates and the track's inner side. Unlike the predecessor, the 900 TT's wheels are now spoked rather than solid to help clear debris from the course. The individual tracks are also modular, which means that if the rubber becomes chunked due to debris contact, it may be changed individually.

The 900 TT is a pleasant ride from Claas, thanks to the four-point cab suspension and completely suspended tracks. The wheels in the tracks, like those on other Claas vehicles with the Terra Trac, are powered by hydraulic pistons.

New Holland PowerStar Tractors range offers unmatched power, comfort, and performance in a UTILITY tractor. They are built for today's jobs with tomorrow's technology.

The PowerStar's long 600-hour service intervals, exceptional fuel economy, and simple daily checks made possible by the one-piece flip-up hood make maintenance a breeze. Engines with four valves per cylinder provide more power and torque to easily tackle all daily duties while lowering fuel bills and pollution. Every model fulfils Tier 4 Final emissions regulations without the need for regeneration, ensuring continuous power throughout the workday.

TYM is offering new tractor models for the North American market as it prepares to break into the top three agricultural brands in the country.TYM's competitiveness is being boosted by the addition of two new tractors with 115 and 130 horsepower.

This is consistent with the present trend in the North American market, where demand for tractors with high horsepower and premium amenities is increasing. The T115 and T130 tractors are high-performance tractors with superior convenience features.

They are outfitted with telematics technology, which gives the operator information on the status of the vehicle, consumables, and work logs. The new tractor even has remote control capabilities.ROOT, a TYM subsidiary that specializes in tractor attachments and machinery, showcased 15 different attachments such as loaders and backhoes for tractors ranging from 20 to 130 horsepower.

Mahindra & Mahindra (M&M) announced a partnership with Jammu & Kashmir Bank to provide loans for tractors and farm machinery. In this context, Mahindra Group's Farm Equipment Sector (FES) has signed an MoU with the lender. J&K Bank will provide financing to prospective Mahindra branded tractors and farm machinery clients through its branches in Srinagar, Jammu & Kashmir, Punjab, Himachal Pradesh, Leh, and Ladakh as part of the cooperation.

"Farmers' ability to use mechanisation solutions on their farms is hampered by a lack of credit. We at Mahindra hope to work with J&K Bank to assist farmers in purchasing the most up-to-date Mahindra farm equipment in the region."

New Holland Agriculture has announced a strategic alliance with Alamo Group's Agricultural Division, a provider of implements and attachments for New Holland's compact and mid-range tractors. Customers of New Holland will be able to finance their new tractor along with their Bush Hog, Rhino, or Schulte-branded attachment at a single low rate thanks to the cooperation.

New Holland dealers can expand their implement selection and offer solutions for a number of applications with complimentary New Holland tractors in one package sale as a result of this relationship. The opportunity to finance jointly through CNH Industrial Capital, CNH Industrial's financial services division, streamlines the purchasing process for New Holland clients.

Technology that will change the vision of the Tractor Industry. India is a significant agrarian economy with almost 50% of its workforce employed in agriculture, but sadly, it is one of the most underutilized sectors. Numerous things have been said and promised, but nothing significant has materialized. Farmers continue to face hardships, and the agriculture industry is plagued by numerous problems.

Low agricultural yield, small-scale mechanisation, growing fertiliser costs, rising fuel prices, and the expensive cost of the newest technologies are a few of these problems. Engineering Services made the decision to enter the agricultural industry with its flagship product, the Hybrid Agri Vehicle (HAV), which was introduced to assist farmers in India.

This decision was made with a strong dedication to giving solutions. With its ground-breaking innovation, this new hybrid vehicle is prepared to transform the lives of farmers.

The Proxecto team displayed its Hybrid Agri Vehicle (HAV) in the famous AgriTechnica in Hanover, Germany, with cutting edge features and cutting edge hybrid technologywhich is the largest trade show for agricultural machinery and equipment in the world. The top professionals in the field responded to HAV quite well.

A large audience of 4.5 lakh visitors, including over 1.3 lakh tourists from throughout the world, grew from an enthusiastic gathering of 2830 exhibitors. Representatives of nations like Spain, Ukraine, Greece, Canada, Argentina, Lithuania, and Belgium filed requests for commercial collaboration in response to HAV, which attracted a great deal of interest from all quarters.

HAV did in fact become the event's main talking point. The hybrid agricultural vehicles received the ideal start thanks to AgriTechnica, which gained widespread attention in the internet and TV media.

HAV is a self-sustaining futuristic tractor that uses economical technology and cutting-edge features. With no gearbox, clutch, battery packs, gearbox or gearbox system, this self-energising hybrid tractor is a true game-changer. It also produces its own electricity for operation.

The ground-breaking electric car boasts an advanced Yanmar engine that provides independent torque management and power, all-wheel independent steering, all-wheel independent suspension, a 2.5 m turning radius, and much more.

Even though the hybrid tractor is presently only offered in S1 (Diesel hybrid) and S2 (CNG hybrid) models, it has the customizability to be converted into an electric tractor that is prepared for the future based on the farmer's needs. As a result of our nation's inadequate infrastructure for electric cars, self-energising hybrid agri vehicles rather than fully electric tractors are currently required.

The revolutionary Hybrid Agri Vehicle is made up of four wheel-mounted electric motors and an alternator capable of delivering electricity directly to the wheel motors via the ECU (Electric Control Unit) without the use of expensive battery packs.

This eliminates any extra mechanical loss and significantly reduces fuel consumption. While its S1 (Diesel hybrid) form may save up to 26 to 30% gasoline, its S2 (CNGhybrid) variation can save up to 50% fuel, making it the most cost-effective farm vehicle. This cutting-edge self-energising tractor is considerably superior than conventional tractors in its pursuit of a better agricultural life for farmers.

It offers sophisticated electric controllers, an interactive touch screen, and an electronic PTO in addition to having all the standard features of a standard 50 horsepower tractor. Additionally, it has a 40 KVA electric power supply unit, maintenance-free performance, safety features, and more. This device can light up to 10 dwellings.

| Sl no | Topic |

| 1 | Market Segmentation |

| 2 | Scope of the report |

| 3 | Research Methodology |

| 4 | Executive summary |

| 5 | Key Predictions of Tractor Market |

| 6 | Avg B2B price of Tractor Market |

| 7 | Major Drivers For Tractor Market |

| 8 | Global Tractor Market Production Footprint - 2024 |

| 9 | Technology Developments In Tractor Market |

| 10 | New Product Development In Tractor Market |

| 11 | Research focus areas on new Tractor |

| 12 | Key Trends in the Tractor Market |

| 13 | Major changes expected in Tractor Market |

| 14 | Incentives by the government for Tractor Market |

| 15 | Private investments and their impact on Tractor Market |

| 16 | Market Size, Dynamics And Forecast, By Type, 2025-2031 |

| 17 | Market Size, Dynamics And Forecast, By Output, 2025-2031 |

| 18 | Market Size, Dynamics And Forecast, By End User, 2025-2031 |

| 19 | Competitive Landscape Of Tractor Market |

| 20 | Mergers and Acquisitions |

| 21 | Competitive Landscape |

| 22 | Growth strategy of leading players |

| 23 | Market share of vendors, 2024 |

| 24 | Company Profiles |

| 25 | Unmet needs and opportunities for new suppliers |

| 26 | Conclusion |

© 2017-2026 Mobility Foresights Pvt Ltd. All rights reserved.

Developed with by ClousTech